This page illustrates the use of xtsteadystate.ado for Stata. See Stata. To download the xtsteadystate package including the ado file type in Stata

-

. net from https://rostam-afschar.de/xtsteadystate

. net install xtsteadystate.pkg

Before running the first set of examples, set up the exemplary dataset by running

-

. webuse nlswork, clear

. local classes 10

. su ln_wage if year==68

. gen class=(r(max)-r(min))/`=`classes'-1' in 1/`=`classes'-1'

. replace class = sum(class) in 1/`=`classes'-1'

. replace class = class-abs(r(min)) in 1/`=`classes'-1'

. xtile category = ln_wage, cutpoints(class)

. mat n = 5

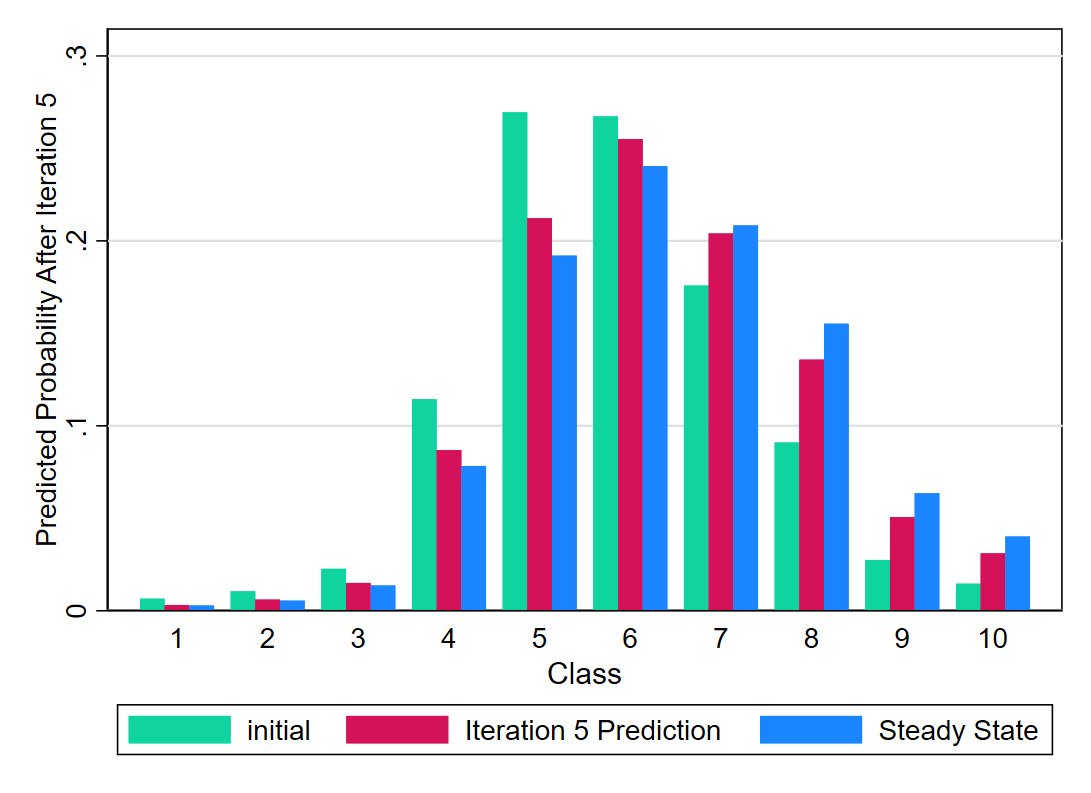

Example 1: Initial, predicted, and steady state wage distributions

-

. xtsteadystate category, bar ini ss pred baropt(bar(1, color("16 212 160")) ///

bar(2, color("212 17 89")) bar(3, color("26 133 255")))

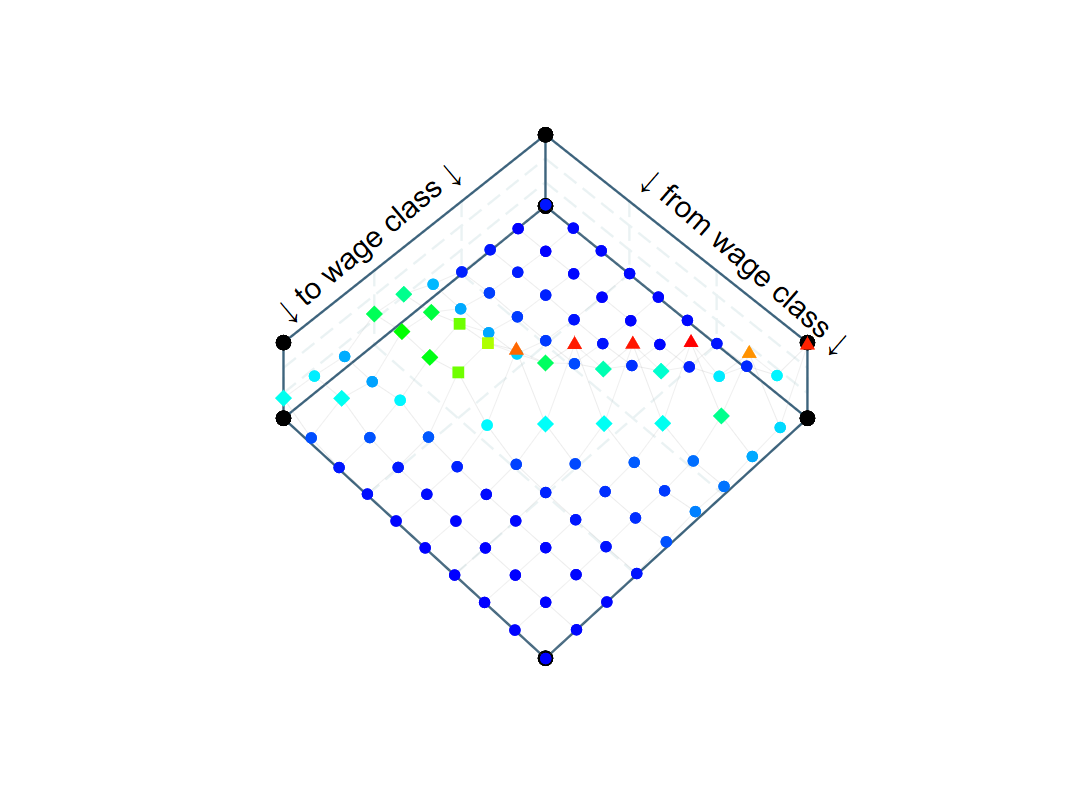

Example 2: Transitions from wage class to wage class

-

. xtsteadystate category, graph3d graph3doptions(yangle(-45) xangle(80) ///

ycam(-4) zcam(-18) cuboid innergrid blv perspective ///

colorscheme(bcgyr) xlabel(" {&darr} from wage class {&darr}") xlpos(1) xlang(-41) zlabel("{&darr} to wage class {&darr}") zlpos(12) zlang(40) wire mark) graph3dscalez(20)

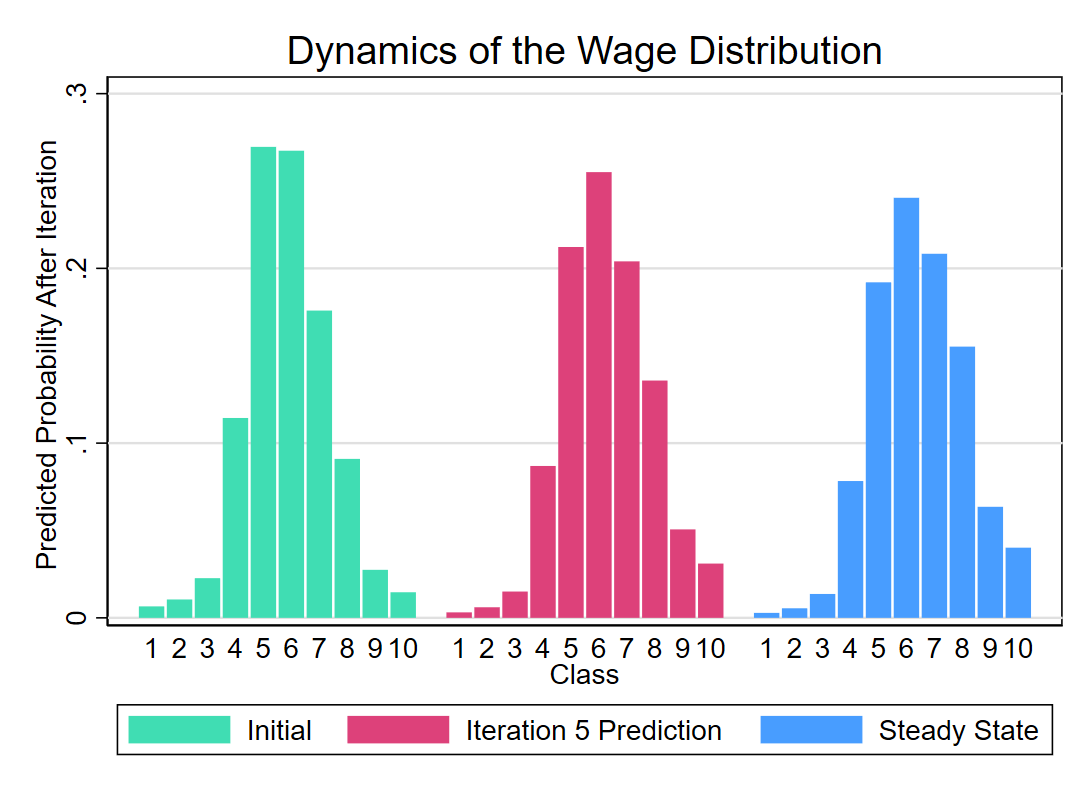

Example 3: Wage dynamics by distribution

-

. xtsteadystate category, tw 3dists ini ss pred ///

twowayopt(title("Dynamics of the Wage Distribution") ///

plotregion(margin(4 4 1)) ylabels(0(0.1)0.3) ///

ytitle("Predicted Probability After Iteration `=`n'[1,1]'"))

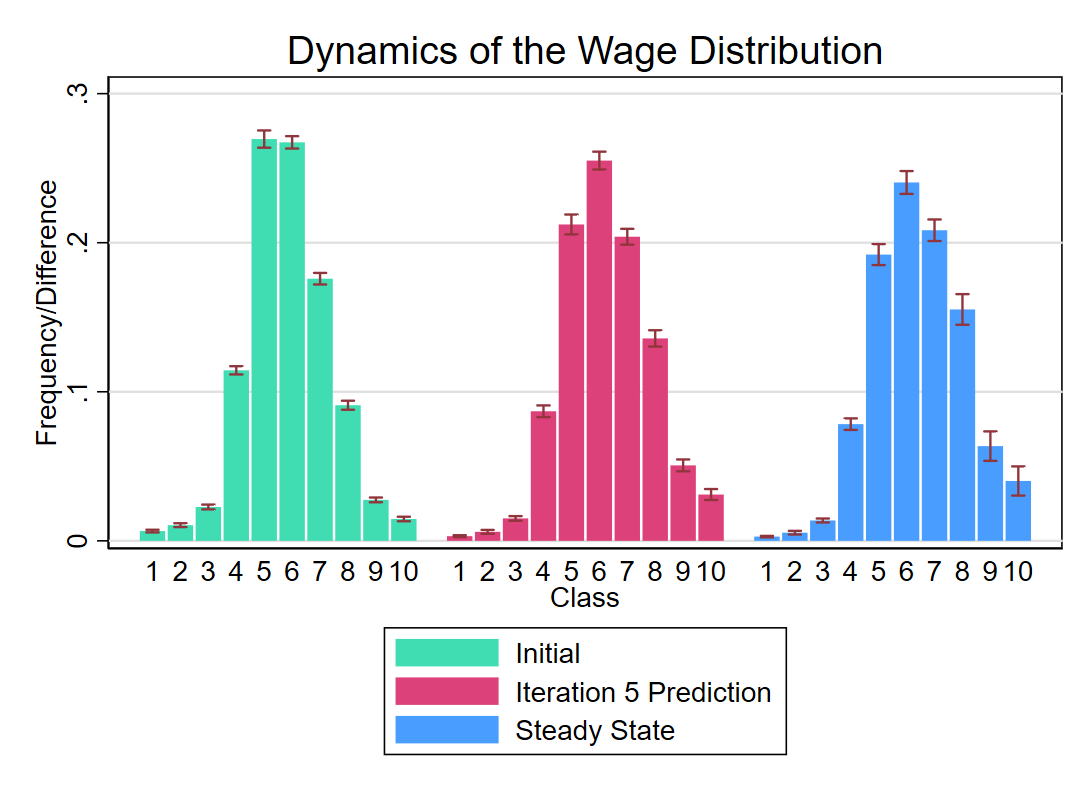

Example 4: Wage distribution dynamics by distribution

with standard errors

-

. xtsteadystate category, boot tw 3dists ini ss pred ///

twowayopt(title("Dynamics of the Wage Distribution") ///

plotregion(margin(4 4 1)) ylabels(0(0.1)0.3) legend(rows(3)))

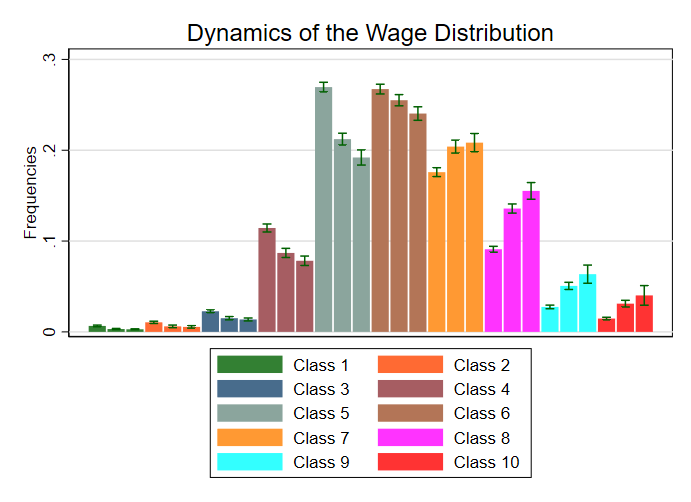

Example 5: Wage distribution dynamics by class

with standard errors

-

. xtsteadystate category, boot tw 1dist ini ss pred ///

twowayopt(title("Dynamics of the Wage Distribution") ///

plotregion(margin(4 4 1)) ylabels(0(0.1)0.3) ///

ytitle("Frequencies"))

Before running the second set of examples, set up the exemplary dataset by running

-

. webuse nlswork, clear

. local classes 4

. su ln_wage if year==68

. gen class=(r(max)-r(min))/`=`classes'-1' in 1/`=`classes'-1'

. replace class = sum(class) in 1/`=`classes'-1'

. replace class = class-abs(r(min)) in 1/`=`classes'-1'

. xtile category = ln_wage, cutpoints(class)

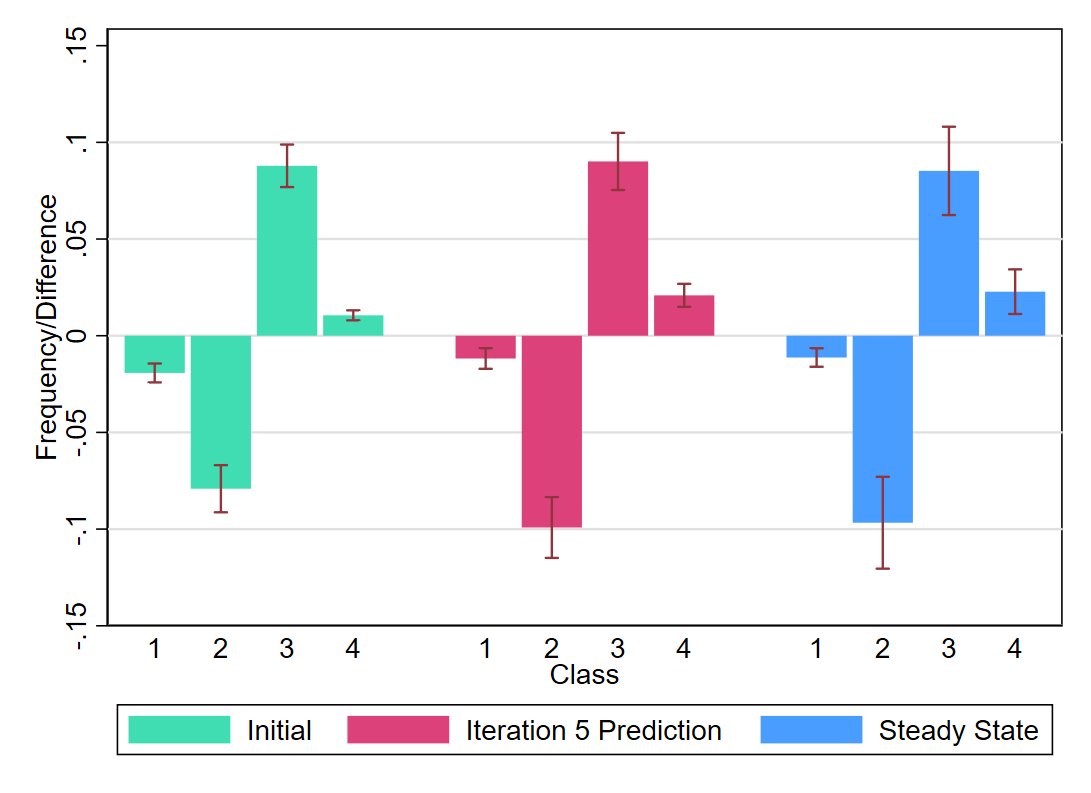

Example 6: Difference in wage dynamics between groups

-

. gen treatment = 0 if race==2

. replace treatment= 1 if race==1

. xtsteadystate category , boot diff 3dists tw ini pred ss ///

twowayoptions(ylabels(-.15(0.05).15))

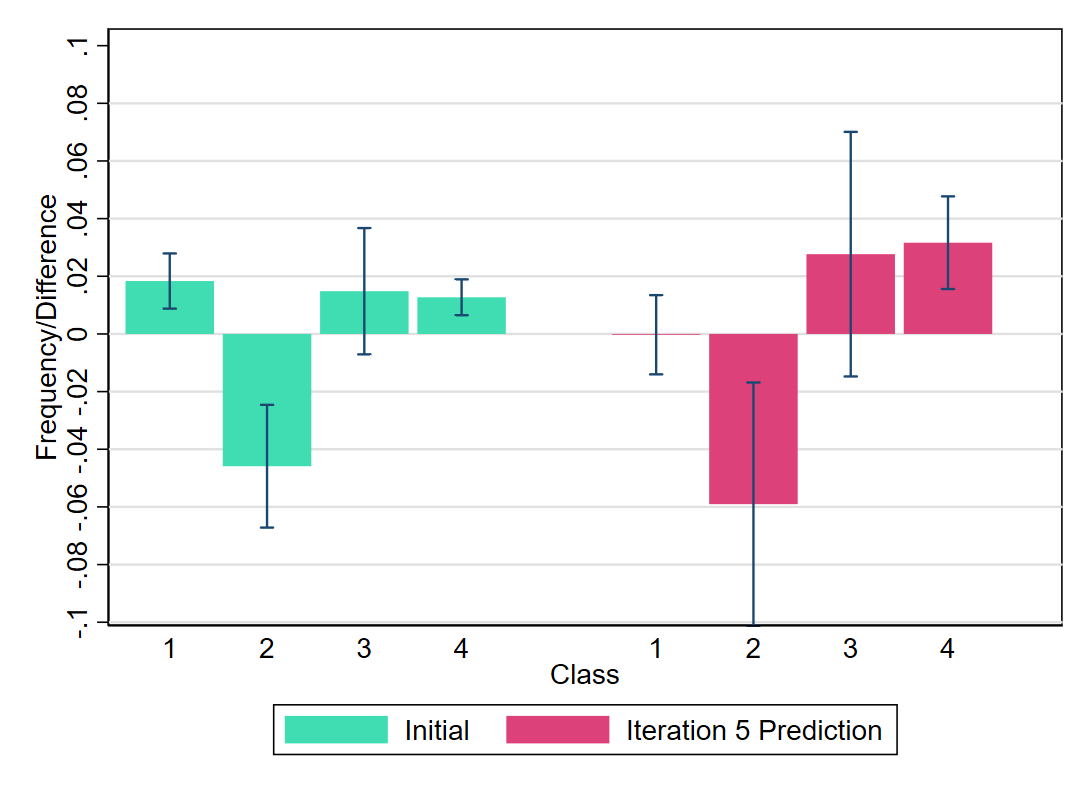

Example 7: Difference in wage dynamics

between groups and over time

-

. gen post= 0 if year<80

. replace post= 1 if year>=80

. xtsteadystate category , boot did 3dists tw ini pred ///

twowayoptions(ylabels(-.1(0.02).1))

Authors

Davud Rostam-Afschar

Universität Mannheim

rostam-afschar@uni-mannheim.de